Wonderful service from start to finish.

What are the different types of de-merger structures?

Making the decision to de-merge your company will be a significant one and choosing the right structure to suit you and your company objectives will require time and the appropriate legal advice. Stacey Browne, Company Commercial Solicitor, explains more here about the five most common de-merger structures, which are direct dividend, indirect de-merger, reduction of capital de-merger, scheme of arrangement and liquidation scheme, reviewing the pros and cons of each structure.

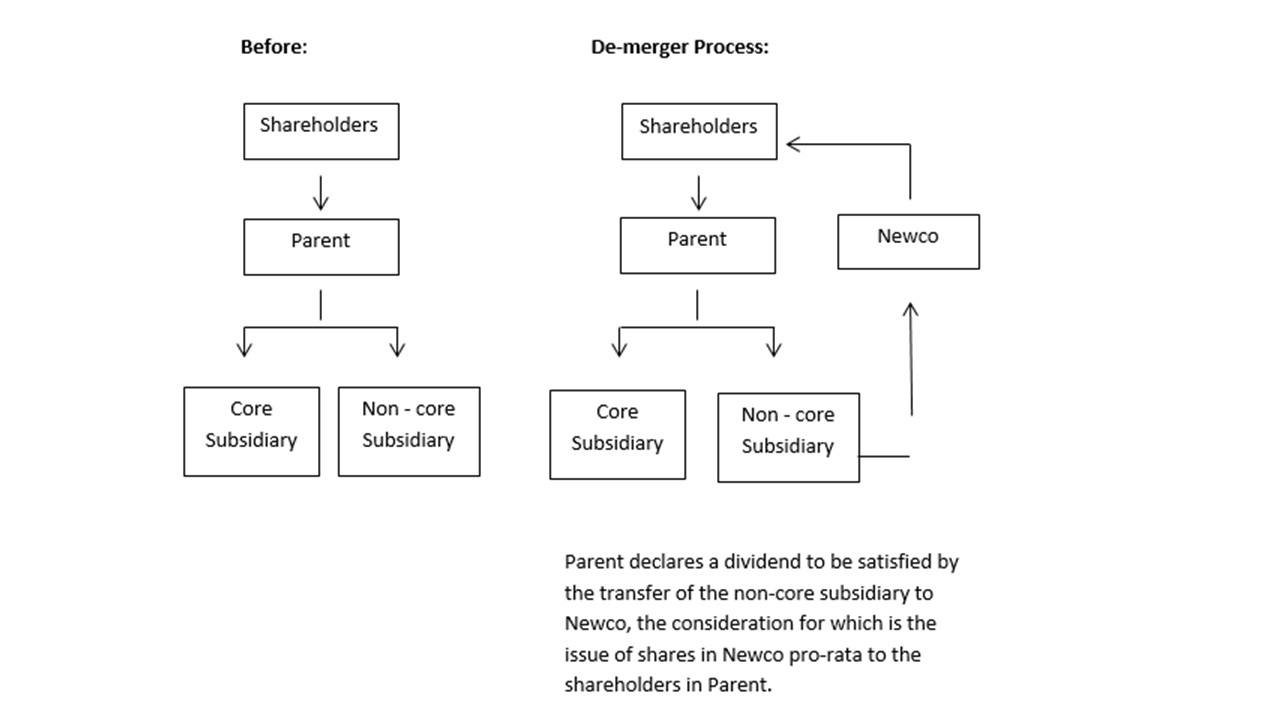

Direct Dividend De-merger Structure

This is the most straightforward, but not usually the most tax efficient, structure for a de-merger. A direct dividend de-merger is effected by the parent company paying to its members a dividend in specie.

This structure is rarely used to de-merge a business or trade because such transfer of the business will constitute an income distribution potentially attracting heavy income tax for shareholders.

The structure would look something like this:

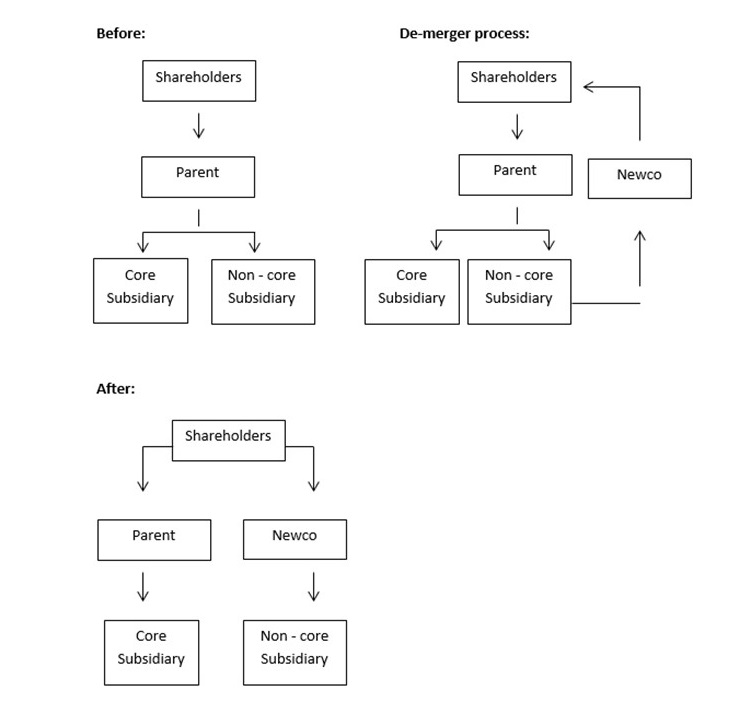

Indirect De-merger Structure

This is a variation of the direct dividend route, above. Essentially, the parent company declares a dividend in specie of either the shares in the subsidiary or the business to be de-merged to a newly incorporated company (newco), or another third party, in consideration for which recipient of the transfer issue of shares directly to the parent’s shareholders.

The structure would look something similar to this:

Reduction of Capital De-merger Structure

This is most relevant to a company that does not have sufficient distributable reserves to declare a dividend in specie or does not want to reduce the amount of its distributable reserves significantly; therefore the de-merger is effected by reducing the capital of the parent company and, in consideration for the reduction of capital, transferring the subsidiary to the de-merged parent’s shareholders (using either assets or shares).

Alternatively, a company might like to reduce its capital and use the reserve arising on the reduction of capital to credit its profits and loss account with a view to using these distributable reserves to declare a dividend in specie.

Similarly to an indirect de-merger, it is also possible to do a triangular reduction of capital by transferring the business to be de-merged to a newco (or third party) that issues shares to the parent's shareholders. To avoid an income distribution, the amount of capital that is cancelled or reduced on the repayment of capital must at least equal the market value of the de-merged assets (as opposed to book value on a direct dividend).

The structure would look something similar to this:

Scheme of Arrangement De-merger Structure

A company can effect almost any kind of de-merger using a scheme of arrangement if the sanction of the court, shareholder approval, and, where necessary, creditor approval is obtained. In practice, a scheme of arrangement will usually be combined with one of the structures described above to effect the de-merger.

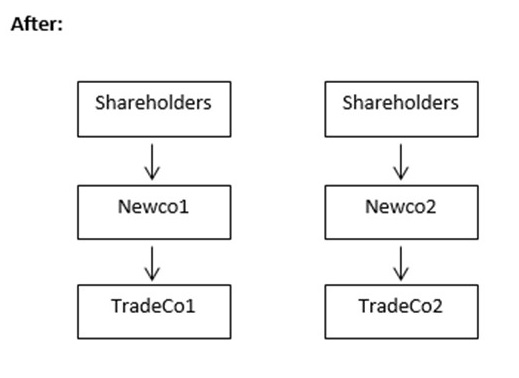

Liquidation Scheme De-merger Structure

This involves the liquidation of the parent company and the transfer of its assets to two or more newly formed companies (newcos) in the following process:

- The liquidator may accept shares in the newcos as consideration for the transfer of the assets from the parent company to the newcos.

- The liquidator distributes these shares to the shareholders of the parent as a dividend in specie as part of the process of liquidating the parent's assets.

- The parent company is then dissolved leaving the two newcos each holding assets of the parent company.

- Sometimes the formal process is simplified by the newcos issuing shares directly to the shareholders of the parent company.

The structure would look something similar to this:

As demonstrated here, there are several different options when de-merging your company, each coming with its own complications and opportunities. As well as seeking the right legal advice, it is always worth checking the tax implications with your accountant / tax advisor before proceeding with any of the detailed structures. To discuss your situation with Stacey or a member of the Company Commercial team, you can call us today on 023 8071 7411 or email staceybrowne@warnergoodman.co.uk.

ENDS

This is for information purposes only and is no substitute for, and should not be interpreted as, legal advice. All content was correct at the time of publishing and we cannot be held responsible for any changes that may invalidate this article.